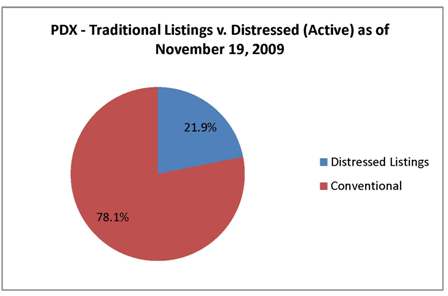

21.9% of listings distressed in PDX, 31.7% in Clark County

The latest report from the Mortgage Bankers Association indicated that the rate of foreclosure for people with fixed rate loans and good credit is on the rise.

The AP reports that homeowners’ inability to keep up with payments is now more due to unemployment, rather than the subprime loans that contributed to the initial increase in foreclosures.

A quick search on RMLSweb reveals that in the Portland Metro area, distressed properties currently make up 21.9% of active residential listings (this number takes into account listings that require third-party approval, as this typically indicates a short sale and those that are marked as bank-owned).

In Clark County, 31.7% of residential listings are distressed.

So the Portland Metro market has a 6.5 month inventory, with 21.9% of those listed as distressed. Since a sustantial number of those distressed properties are short sales waiting for lender approval, that would indicate to me that the actual inventory is actually less than 6.5 months and could be as low as 5.1 months when those distressed properties (which are not really available for sale) are taken out of our statisics. I’m including bank owned properties under the “not available for sale” category since many of them are cash only, not financeable. The actual available inventory may be even lower, since not all listings are updated yet with the short sale fields (from what I understand after reading RMLS news). Why isn’t this news?

Re: previous comment… If you are going to adjust the months of inventory ratio by subtracting the properties requiring third party approval, perhaps you should also add the various components of the shadow inventory that do not show up in MLS stats to begin with, such as REOs held by banks but not listed for sale and delinquent properties not yet foreclosed upon due to foreclosure moratoria, HAMP, loan mods, etc.

On the other side of this equation (monthly number of sales), a lot of properties are counted twice when they are sold to cash investors first and then quickly resold to their eventual owner, often with the use of new subprime/FHA loan products.

All thing considered, months of inventory is a pretty meaningless number by which to gauge the state of the RE market. For examples, in Las Vegas months of inventory have now been falling for 20 (yes, twenty) consecutive months. Yet prices still keep falling as indicated by the September Case-Shiller index released earlier this week. PDX prices have also fallen in September after three months of rather anemic growth. It makes more sense to watch lead indicators, such as the number of NOD’s and trustee sales. Those will have to peak before the prices bottom out.

Could you please be clearer when stating your numbers, what ALL of the parameters you used are? How are you defining Portland (city, MLS areas – if so, which ones – zip codes?), residential only or residential and multi-family or all property types?, active and bumpable or only active? Did you really use the 3rd party approval field? Doesn’t the 3rd party approval also include sales by estates and trusts, which may or may not be distressed? Isn’t that why RMLS created the separate short sale field so that members would be able to accurately discern which listings were actually short sales and which were estates? Do bank owned homes really have the 3rd party approval field checked? Aren’t they the sellers at that point so no 3rd party approval?

Hi Kris – the geographic parameters are the same as used in Market Action. Portland is areas 141-156 (Clackamas, Columbia, Multnomah, Washington and Yamhill) and Clark County is areas 11-72. I ran these numbers only for residential properties and did include active and bumpable listings.

In this case, I did use 3rd party approval as an indicator of short sales & not the short sale field. The reason I did so is that only 93% of active listings have had the short sale field updated since we added it. Once that number is closer to 100%, we will use the short sale field for any statistics about short sales. But at the time I ran these, we still felt the 3rd party approval field is a better indicator of the true number of short sales.

As far identifying bank-owned homes goes, I used the bank-owned field.

Hope this helps answer your questions. Thanks!

Thanks for the clarification. It’s important that people, particularly journalists, know the parameters when stats are quoted. Even then, some people will still take them out of context but if at least the original source has them, people can find out what’s what.

I am trying to view properties on rmls.com,quick search but it says my min. value should be lower than my max. value. I checked and it was in the boxes correctly. Can you please help me.

Thanks, Joan Reeves

Hi Joan, can you let me know what the exact Search Criteria you’re using for each field? That way, we can see if we can recreate the problem. You can reply to this message or e-mail communications@rmls.com.

Thanks!