![Residential Distressed Properties for January – March 2012]()

by RMLS Communication Department | May 3, 2012 | Industry News, Market Trends, Statistics

This chart shows the number of Bank Owned and Short Sales in all areas of the RMLS™ system during the first quarter of 2012. To download or print the chart, click here.

Below are links to additional charts for some of our larger areas*:

Portland Metro

Clark County, WA

Lane County, OR

Douglas County, OR

*If you want information on percentages of distressed residential sales in other areas not represented by our charts, please contact us at communications@rmls.com.

Here are some additional facts about distressed residential properties in the first quarter of 2012:

All Areas when comparing percentage share of the market 1st quarter of 2011 to 1st quarter of 2012

- When comparing the first quarter of 2011 to 2012, distressed sales as a percentage of new listings decreased by 0.6% (29.5% v. 28.9%).

- In a comparison of the first quarter of 2011 with the same period in 2012, distressed sales as a percentage of closed sales decreased by 2.0% (40.9% v. 38.9%).

- Short Sales comprised 15.0% of new listings and 13.0% of sales in 2012, down 0.2% and up 2.7% from first quarter 2011, respectively.

- Bank Owned properties comprised 13.9% of new listings and 25.9% of sales in first quarter 2012, down 0.4% and up 4.7% from 1first quarter 2011, respectively.

Portland Metro when comparing percentage share of the market 1st quarter of 2011 to 1st quarter of 2012

- When comparing the first quarter of 2011 to 20112 distressed sales as a percentage of new listings decreased by 0.5% (31.5% v. 31.0%).

- In a comparison of the first quarter of 2011 with the same period in 2012, distressed sales as a percentage of closed sales decreased by 2.5% (41.7% v. 39.2%).

- Short Sales comprised 16.1% of new listings and was down 0.2% from 2011. However, the percentage of sales rose from 9.9% in 2011 to 13.5% in 2012, a 3.6% rise.

- Bank Owned properties comprised 14.9% of new listings and 25.7% of sales in first quarter 2012, down 0.3% and 6.1% from 2011, respectively.

Clark County when comparing percentage share of the market 1st quarter of 2011 to 1st quarter of 2012

- When comparing the first quarter of 2011 to 2012, distressed sales as a percentage of new listings decreased by 4.6% (39.7% v. 35.1%).

- In a comparison of the first quarter of 2011 with the same period in 2012, distressed sales as a percentage of closed sales increased by 0.3% (47.8% v. 48.1%).

- Short Sales comprised 23.8% of new listings and was down 0.6% from 2011. However, the percentage of sales rose from 17.1% in 2011 to 20.4% in 2012, a 3.3% rise.

- Bank Owned properties comprised 11.3% of new listings and 27.7% of sales in 2012, down 4.0% and 3.0% from 2011, respectively.

by RMLS Communication Department | Sep 22, 2011 | Industry News, Market Trends, Statistics

See a visual representation of distressed properties in our market!

Last May, we debuted new infographics to show how distressed properties identified as Short Sales and Bank Owned were represented in the 2010 housing market. Now, we’re pleased to present new infographics on distressed properties for the first two quarters of 2011! When compared with the data from 2010, these stats offer a more comprehensive picture of how the local housing market has changed in the past year and a half.

(Click the image to enlarge.)

The above infographic shows a visual representation of the number of Bank Owned and Short Sales in all areas of the RMLS™ system during the first half of 2011. The top half shows new listings and sales from January through June 2011, while the bottom half shows new listings and sales by quarter. To download or print the infographic, click here.

Below are links to additional infographics for some of our larger areas*:

Portland Metro

Clark County, WA

Lane County, OR

Douglas County, OR

*If you want information on percentages of distressed sales in other areas not represented by our infographics, please contact us at communications@rmls.com.

As can be seen from the above infographic, the percentage of distressed sales in the overall housing market increased for closed sales compared with new listings. However, the amount of short sales decreased as a percentage of closed sales versus new listings, while the amount of bank owned properties greatly increased.

The quarterly trend shows a decrease of new listings that were distressed, when comparing Quarter 1 with Quarter 2. Distressed sales also decreased as a percentage of closed sales in a comparison of Quarter 1 and Quarter 2. This trend remains consistent with the data from Quarters 1 and 2 from 2010.

Here are some additional facts about distressed properties in the first half of 2011:

- In a comparison of the first half of 2010 with the same period in 2011, distressed sales as a percentage of new listings increased by 4.5% (20.9% v. 25.4%).

- In a comparison of the first half of 2010 with the same period in 2011, distressed sales as a percentage of closed sales increased by 9.9% (28.1% v. 38%).

- Short Sales comprised 13.4% of new listings and 10.1% of sales in 2011, up 2.1% and 1.1% from 2010, respectively.

- Bank Owned properties comprised 12.1% of new listings and 27.9% of sales in 2011, up 2.4% and 8.8% from 2010, respectively.

by RMLS Communication Department | May 2, 2011 | Fun Facts, Homeownership, Market Trends, Statistics

See a visual representation of distressed properties in our market!

One request we’ve frequently gotten from subscribers is to display data on Short Sales and Bank Owned properties. As a result, we have created brand new infographics to show how distressed properties identified as Short Sales or Bank Owned were represented in the 2010 housing market. This is the first report in an ongoing series that will show you how our local market has been affected by the economic downturn.

(Click the image to enlarge)

The above infographic shows a visual representation of the number of Bank Owned and Short Sales in all areas in the RMLS™ system during 2010. The top half shows new listings and sales for the entire year, while the bottom half shows new listings and sales by quarter. To download or print the infographic, click here.

Below are links to additional infographics for some of our larger areas:

Portland Metro

Clark County, WA

Lane County, OR

Douglas County, OR

*If you want information on percentages of distressed sales in other areas not represented by our infographics, please contact us at communications@rmls.com.

As can be seen from the above infographic, the percentage of distressed sales within the overall housing market greatly increased in closed sales compared to new listings. Additionally, the amount of Short Sales decreased by more than a third when comparing closed sales with new listings. The quarterly trend shows an increase of new listings which were distressed, particularly in Quarter 3 and Quarter 4. Looking at sales, Quarter 2 and Quarter 3 both show decreases in distressed sales compared to Quarter 1, and Quarter 4 ended with only a 0.1% rise in distressed sales compared with Quarter 1.

Here are some additional facts about distressed properties in 2010:

- Distressed properties comprised 24.1% of new residential listings, and 29.3% of residential sales.

- Short Sales were 11.8% of new listings, and 8.9% of sales.

- Bank Owned properties were 12.3% of new listings, and 20.4% of sales.

by RMLS Communication Department | Feb 23, 2011 | Market Trends, RMLS News, Statistics

Now including new Affordability documents!

Did you know our Statistical Summaries have been updated with data from 2010? We’ve also added new documents in the Portland, SW Washington, and Lane County folders to show our affordability graphs, which previously only appeared in our Market Action reports the first month of every quarter. Subscribers requested that we make the affordability graphs more accessible, which is why we created these new documents. Now, you no longer have to search through old Market Action reports to find the Affordability Index!

Did you know our Statistical Summaries have been updated with data from 2010? We’ve also added new documents in the Portland, SW Washington, and Lane County folders to show our affordability graphs, which previously only appeared in our Market Action reports the first month of every quarter. Subscribers requested that we make the affordability graphs more accessible, which is why we created these new documents. Now, you no longer have to search through old Market Action reports to find the Affordability Index!

The new Affordability documents are for Lane County, the Portland Metro area, and SW Washington, and can be found in the three areas’ respective Statistical Summary folders. Unfortunately, we do not have Affordability information available for any other areas due to limited median income information from HUD.

To find the new Affordability documents or see the updated Statistical Summary documents on RMLSweb, here is where they are located:

1. Go to Forms and Documents (via Toolkit).

2. On the left side of the screen in Forms and Documents, you will see the Folder Menu with yellow folder files.

3. Go to the folder called 1500-1699 Market Action and Statistics Menu.

4. If there is a “+” sign next to the folder, click it to open the Market Action and Statistics Menu folder. If there is a “-” sign, it is already open.

5. The Statistical Summaries are grouped by area, and can be found in the folders between 1520 and 1699.

6. The new Portland Metro Affordability document can be found in folder number 1520-1539.

7. The new SW Washington Affordability document can be found in folder number 1549-1559.

8. The new Lane County Affordability document can be found in folder number 1560-1579.

by RMLS Communication Department | Nov 17, 2010 | Industry News, Market Trends

How does this affect Washington and Oregon?

A new Brookings Institute study predicts the future of real estate is in “walkable cities,” described as, “walkable, accessible communities with convenient transit linkages and good public services like libraries, cultural activities, and health care.” This is good news for Oregon and Washington, an area of the country particularly rich with interesting, walkable (and bikeable, of course) towns!

According to the report, the new real estate boom will come from the “Millennial” generation, or the kids of the Baby Boomers, born between 1977 and 1994, who amount to 76 million of our country’s population. (Full disclosure: I am one of those 76 million.) The report claims that Millennial aspirations “have been informed by ‘Friends’ and ‘Sex in the City’, shows set in walkable urban places, as opposed to their parents’ mid-century imagery of ‘Leave It to Beaver’ and ‘The Brady Bunch,’ set in the drivable suburbs.” (Unfortunately, the above examples of ‘Friends’ and ‘Sex in the City’ don’t quite match the ideal, walkable, transit-oriented neighborhoods described elsewhere in the report, since both shows were set in New York City. But that’s beside the point.)

According to the report, the new real estate boom will come from the “Millennial” generation, or the kids of the Baby Boomers, born between 1977 and 1994, who amount to 76 million of our country’s population. (Full disclosure: I am one of those 76 million.) The report claims that Millennial aspirations “have been informed by ‘Friends’ and ‘Sex in the City’, shows set in walkable urban places, as opposed to their parents’ mid-century imagery of ‘Leave It to Beaver’ and ‘The Brady Bunch,’ set in the drivable suburbs.” (Unfortunately, the above examples of ‘Friends’ and ‘Sex in the City’ don’t quite match the ideal, walkable, transit-oriented neighborhoods described elsewhere in the report, since both shows were set in New York City. But that’s beside the point.)

Rest assured: this study does not mean that Millennials will flock to Portland and abandon Oregon’s smaller towns. In fact, the report uses as a prime example Utah’s preparations for the 2002 Winter Olympics in Salt Lake City. In addition to building up Salt Lake City, Utah built up the entire surrounding four-county area to create a large variety of “dense walkable neighborhoods built around transit stops.” Additionally, Portland is used as an example of transit directly benefitting real estate, stating that the city’s decision to spend $50 million on the downtown streetcar created $3.5 billion in private-sector development around the streetcar lines.

The best news in the report simply counteracts the onslaught of bad housing news the media seems to focus on these days. Simply put, when the Millennials begin buying houses, they will constitute the largest market of first-time homebuyers in history. This is good news for everyone. Similarly, with a focus on public transit and less of a reliance on personal cars, homeowners will have more cash on hand. The study cites an astonishing figure: Cutting one car out of the typical household budget can allow that family to afford a $100,000 larger mortgage.

The best news in the report simply counteracts the onslaught of bad housing news the media seems to focus on these days. Simply put, when the Millennials begin buying houses, they will constitute the largest market of first-time homebuyers in history. This is good news for everyone. Similarly, with a focus on public transit and less of a reliance on personal cars, homeowners will have more cash on hand. The study cites an astonishing figure: Cutting one car out of the typical household budget can allow that family to afford a $100,000 larger mortgage.

Overall, this spells good news for Oregon and Washington, which contain a wide variety of interesting, green communities (both large and small) that greatly appeal to Millennials. As this generation begins to wade into the housing market, the future of the real estate market in the Pacific Northwest looks very hopeful.

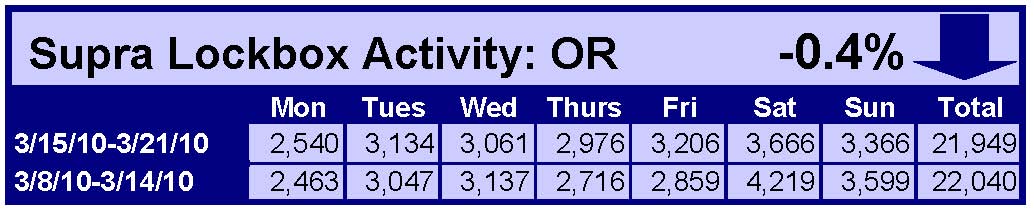

by RMLS Communication Department | Mar 29, 2010 | Industry News, Lockbox, Market Trends, Oregon Real Estate, Statistics, Supra, Washington Real Estate

Minimal changes from previous week

When comparing the week of March 15-21 with the week prior, the number of times an RMLS™ subscriber opened a Supra lockbox increased 1.0% in Washington and decreased 0.4% in Oregon.

Click the chart for a larger view

Archive

View an archive of the Supra lockbox statistical reports on Flickr.